ArcelorMittal Reports Q2 2025 Results; Highlights Margin Gains, Strategic Expansions

ArcelorMittal has announced its financial and operational results for the second quarter and first half of 2025, showcasing sustained improvement in margins, robust operational performance, and progress in strategic growth initiatives.

Q2 2025 key highlights:

Safety focus: Protecting employee health and safety is a core value of the Company. LTIF rate of 0.68x in 2Q 2025. dss+ safety audit recommendations implementation phase is underway.

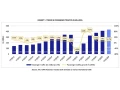

Sustained margin improvement: Despite continuous challenges, the Group’s results show the benefits of (i) asset optimization, (ii) regional and end market diversification, and (iii) strategic growth investments. 2Q 2025 EBITDA of $1.9bn, with a margin of $135/tonne that continues to show improvement vs. prior cycles. Net income of $1.8bn in 2Q 2025 (EPS of $2.35/sh) was positively impacted by $0.8bn exceptionals (net of impairments and tax effects)4. Adjusted net income of $1.0bn in 2Q 2025 (adjusted EPS of $1.32/sh)4.

Operational momentum continues: Record quarterly iron ore production and shipments from Liberia, which remains on track to achieve its full expanded 20Mt capacity by end 2025; first slab cast at Calvert's new 1.5Mt EAF in the U.S.; India renewables reaching industrial scale and value add capacity commissioning underway.

Financial strength maintained: Net debt of $8.3bn at the end of the quarter, with the increase of $1.5bn from the prior quarter end due largely to M&A impacts following the full consolidation of AM/NS Calvert, Tuper and ArcelorMittal Tailored Blanks Americas (AMTBA), which combined are expected to support higher normalized EBITDA of circa $0.3bn; liquidity remains at a robust $11.0bn7; during the quarter, S&P upgraded the Company’s credit rating to BBB (from BBB-).

Cash flow being reinvested for growth: Over the past 12 months, the Company has generated investable cash flow6 (net cash provided by operating activities less maintenance/normative capex) of $2.3bn. Over the same period, the Company has invested $1.1bn in strategic capex projects to enhance long-term EBITDA capacity, returned $1.1bn to shareholders via dividends/buybacks, and allocated a net $2.3bn to M&A.

Key developments towards strategic objectives

Growth: ArcelorMittal has completed the acquisition of Nippon Steel’s 50% stake in AM/NS Calvert, gaining full control of one of North America’s most advanced steel making facilities. Calvert’s new 1.5Mt EAF, the first of its kind designed to supply exposed automotive grades, has been successfully commissioned, with the first slabs cast during the quarter. Together with a new 7-year slab supply agreement signed with NSC/USS, this ensures Calvert’s needs for U.S. “domestically melted and poured” material. Additionally, ArcelorMittal acquired control of the Brazilian pipe producer Tuper (a JV in which it already held a 40% interest) and regained control of AMTBA to accelerate growth in high-value tubular and automotive markets in North America.

Organic growth: The Group's strong financial position enables the consistent funding of organic growth projects to support future profitability and investable cash flow. The Group‘s high return strategic growth projects, together with the impact of recent M&A, are expected to increase future EBITDA potential by $2.1bn6. The EBITDA benefit targeted for 2025 is $0.7bn, of which $0.2bn was captured in 1H 2025 EBITDA.

Encouraging EU trade policy momentum to restore fair competition: the “Steel and Metals Action Plan” recognizes the factors needed to restore industry competitiveness; an effective carbon border and more efficient trade measures that limit import penetration to historical levels have the potential to support improved domestic steel capacity utilization rates and restore the industry’s health. It is imperative that these plans are swiftly turned into concrete actions, with announcements anticipated in 2H 2025 on the details of the new tool that will replace the current safeguard measures and a proposal to close major loopholes in the Carbon Border Adjustment Mechanism (CBAM).

Consistent shareholder returns: As per its capital allocation and return policy, in addition to its growing base dividend ($0.55/sh, paid in 2 equal instalments), the Company will continue to return a minimum of 50% of post-dividend annual free cash flow to shareholders. Since September 20205, the Company has used buybacks to reduce its fully diluted shares outstanding by 38%. So far in 2025, the Company has repurchased 8.8m shares at a total cost of $262m.