India Ratings Maintains Stable Outlook for Large Corporates in 2HFY26

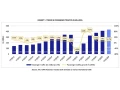

India Ratings and Research (Ind-Ra) has maintained an overall Stable rating Outlook for large corporates (LCs) for 2HFY26. This is in view of 82% of the rated portfolio being on a Stable Outlook as of 31 August 2025, largely unchanged over the past year.

“Tariff shocks notwithstanding, majority LCs have healthy balance sheets, stable cash flow outlook and easing liquidity conditions. While modest demand growth may limit broad basing of capex, consolidation in competitive sectors and global value chain opportunities would keep M&A momentum healthy. Caution is advised for a few export-heavy sectors such as textiles which remain vulnerable to near-term trade volatility,” Abhishek Bhattacharya, Head - Large Corporate Ratings, Ind-Ra.

While LC balance sheets are healthy, the demand slowdown has caused lingering stress for job-intensive small and medium enterprises (SMEs). These sources of sectoral stress for LCs and SMEs can be bucketed into three broad themes: 1) In domestic consumption-driven sectors (such as auto, FMCG, real estate (RE)), K-shaped recovery persists, impacting the value chains exposed to the lower jaw of recovery; 2) A subdued growth outlook in infrastructure spending has intensified competition in certain sectors, driving margin erosion in EPC, cement and telecom-media; and 3) recent geopolitical shocks, including US tariffs have created significant vulnerability for export-led sectors (such as textiles, diamonds, and select agro-commodities). However, in some commodity driven sectors (such as metals and jewellery), SMEs are likely to be more severely impacted by external shocks than LCs, as the latter cater to primarily domestic demand, have a diversified customer profile and have benefited from the recent deleveraging cycle.

Consequently, Ind-Ra has maintained a deteriorating outlook on sectors namely road EPC, Tier-2 cement players and Tier-2 residential RE players for 2HFY26. The agency has also revised the outlook on the textiles and cut & polished diamonds (CPD) sector to deteriorating from neutral. Tariff uncertainty is likely to impact earnings and cash flows for 2HFY26 for LCs in export-heavy sectors, along with an increase in the working capital cycle. Most well rated LCs have ample liquidity, nimble supply chains to mitigate potential demand slowdowns, and have seen cash flow boost from preponed orders. However, in the textile sector, 25% of corporates will have limited headroom to navigate ongoing disruptions.

While the overall capex recovery remains uneven, corporates with robust balance sheets continue to invest in brownfield capacity expansion and inorganic opportunities. Ind-Ra expects sectors such as power, telecom, oil & gas, and metals to drive bulk of ongoing capex. New sectors namely data centres, warehousing, semi-conductor value chains and electric mobility would grow in significance, aided by government incentives and Production-linked Incentive schemes. Market consolidation by the top players in cement, EPC, realty, logistics and healthcare is likely to continue. Auto ancillaries, chemicals and pharma players would continue to pursue strategic M&A opportunities to deepen their footprint into global supply chains. However, broad-based pickup in capex and traction on greenfield expansion are likely to get pushed out with overall investment growth hovering around mid-single digits.

While banks sit on significant liquidity, capital markets continue to provide lower cost opportunities for high-rated corporates. For lower-rated corporates within working capital-heavy sectors such as EPC, chemicals, and textiles, access to timely funding would remain a monitorable. Working capital requirements could increase in 2HFY26 for export-heavy sectors. Also, softening equity market sentiments are likely to weigh on corporates planning to deleverage through capital raising. Ind-Ra would remain cautious on corporates’ heavily dependence on fund raising plans for FY26/FY27.